How to Teach Kids About Money: 20 Practical Tips for Every Age

Updated on July 10, 2026

Key Points: Teaching kids about money doesn’t have to start with big lectures about bank accounts, debt, or investing. You can start teaching your kid about finances with simple daily moments like comparing costs in a supermarket and talking about why you buy one thing and wait for another. Here are 20 practical tips for teaching kids financial literacy, organized by age, to help you apply them. At this age, the core money skills for children are understanding that money is used to buy things, that money can run out, and that sometimes people wait before buying something they want. A piggy bank is quite common for savings, but a clear jar is even better for younger kids, as they can see the money amount actually grow. To speed up the development of financial literacy for kids, you label the jar with simple goals like a toy car or a new set of crayons. Keep the goals simple, as young kids need quick wins. Young kids often see their parents tap cards or phones, especially in this digital age, but they don’t always understand that that’s how you are spending money. So, when teaching kids about money, it’s important to make payments more visible. You can use cash instead, whenever possible, or, when in the store together, tell them how much each item costs. You don’t need to explain your whole family budget; just make sure you know that when you get something, you exchange money for it. “In our 'credit card economy,' money can feel limitless.” Use toys, snacks, and books to set up a little store at home. Then, give your kids pretend money or real coins (of the same value), and let them buy items from you. You can keep it simple. Apple is one coin, a toy is two coins, a book is three coins. Make sure they don’t have enough coins to buy everything, so that they think about their needs vs. wants. “For preschoolers, introducing money is best done through play rather than focusing on dollar amounts or value.” Children learn what they see, so when teaching money management for kids, you need to be a mindful spender yourself. If your child sees you pause before buying something, compare prices, or hears you say that you are saving up for something, they begin to understand the existence of money choices. This also teaches kids delayed gratification and that sometimes they need to wait before buying to get something better later. Learn exactly how Brighterly helps students thrive through expert sessions, online tools, and proven feedback from thousands of satisfied parents By this point, your kid understands counting money and comparing prices, and now it’s time to teach them about careful spending, saving, and giving. Understanding needs vs. wants is one of the first big ideas in financial education for children, and it will shape your kid’s financial future. You can teach this in many ways. For example, when in the store, ask your child if different items are needs or wants. The lesson isn’t that wants are bad, but that needs come first. A commission system means that your child earns money by doing age-appropriate chores beyond their usual family responsibilities. For example, you expect them to make their bed, so it’s not paid. But helping with washing the car or watering plants may be an additional chore through which they can start earning money. Saving money for kids becomes more exciting if they have a concrete goal. The clear jar is a good starting point, but as your kid gets older, you can set a larger goal together. It can be a book, a ticket to a sports event, or a gift for a friend. Then, depending on the price, help them work out how much they need to save. For example, if a new toy costs $20, and they can save up $5 per week, they will need four weeks. “In our house, turning eight means graduating from participating in picking out a friend's birthday gift to funding the purchase as well.” Children, like adults, practice opportunity cost every time they make a money choice. The $5 they spent on snacks is $5 they can no longer spend on a toy. Explain to them that while both choices are okay, they cannot spend the same money twice. Impulse buying is hard to manage for kids and adults alike. Suggest a simple rule: a child needs to wait for 24 hours before buying something unplanned. Chances are, they will forget the item quite quickly. If they don’t, discuss whether the purchase aligns with their savings goal. At this stage, you should also teach your kids that they can use their money to help others. Ask them to put a few coins a week away for the local animal shelter, a school fundraiser, or any other cause they care about. The amount doesn’t have to be large; what’s important is developing the habit of charitable donation. Note: To develop healthy money habits, children need to have a strong number sense. If you think your child needs more support with early math skills, our 1st grade math, 2nd grade math, and 3rd grade math programs can help them get better at understanding numbers and using them for real-life problem-solving.

Help your child build real-life math confidence through 1:1 lessons with experienced tutors.

At this age, many kids start buying things online and noticing what their friends have. So, knowing how banking, budgeting, and compound interest work starts to matter. With a bank account, your kid can now see how their money moves in and out of their account. A simple savings account (or a joint one), or a youth account, if your bank offers one, are good places to start. Sit with your kid and explain to them what the numbers in their bank app, like balance, deposit, and interest, mean, so they can keep track of their money safely. Budgeting for kids doesn’t have to be complicated. You can help your kid to track income and spending for one month. If they don’t yet have a bank account, you can create a basic three-column list containing places for income, planned spending, and actual spending. During the month, once they make a purchase or donation, they should record it in the “spent” category, and you can review it at the end of the month. Middle schoolers are mature enough to understand compound interest. The idea is that money can earn more money over time. For example, if they put $100 in an account earning 5% per year and leave it alone, in 10 years it will be $163. Explain to them that the initial growth is small, but as the amount in the bank account grows, so do the earnings. Note:You don’t need to go too deep into multiplication and addition formulas. The main lesson here is that money can earn money, and starting early matters. The core idea you need to explain is that instead of spending all their money now, one can put it into something that grows over time. Bring examples of stocks of companies they already know, and how having stocks means having a small ownership share. If the company grows, its share may become worth more. If the company struggles, it may lose value. Keep the message balanced, as investing isn’t a guaranteed way to earn money. You can also connect investing to math. Understanding percentages, graphs, and patterns will help them understand investment and growth better. Note: If your child is starting to struggle with ratios, variables, or early algebra topics, our pre-algebra tutors can help them build the math foundation they need for financial literacy. By middle school, your child will be aware of what other kids have. This social comparison stage can make impulse buying much harder to deal with. This is why contentment is a big part of how to teach kids about money. Kids need to learn that they don’t need to buy something just because someone else has it, and waiting till they can afford something is an investment for later. 74% of the US teens report not being confident in their financial education (Moneyzine, 2024). At the same time, your teenager is close to the stage in life when they will start making real financial choices on their own. At this stage, teaching kids about money means, above all else, responsibility and planning. When your kid starts working, they will start to understand the time and effort it takes to earn money, as well as things like taxes and schedules, in a more real way. Working also changes spending habits, as every purchase will represent several hours of their work. By ages 14-16, your teen will probably be ready to manage their own credit card and checking account. This way, they can learn how to track deposits, use a debit card, check their balance, and avoid spending more than they have. Most importantly, let small mistakes happen, and don’t step in every time they misstep, so they learn to handle those themselves. “One of the most important lessons I teach, both professionally and as a parent, is that money is something you participate in, not something that just appears or disappears.” Credit cards can be useful tools, but they come with risks, too. If your teen doesn’t know about these risks, they may develop credit card debt without even noticing it. The biggest danger here is thinking of credit as extra money. Instead, credit is borrowed money that your child will need to pay back, with interest. Even small amounts can pile up into big numbers, leading to a debt spiral, and it’s important your child knows this. If your child has already earned money from a part-time job or a side hustle, it’s time to introduce them to a Roth IRA. A Roth IRA is a retirement account where the money can grow over the years. According to the IRS official website as of May 2026, if people have taxable compensation and meet the income rules, they can contribute to a Roth IRA. For teens, this means income from work, and not gift money or allowance for kids. College is likely the largest financial decision your teenager will face before they turn 25. You need an honest, but age-appropriate, conversation about student loans, scholarships, housing costs, and part-time job options. Explain that college can be paid for in different ways, using scholarships, savings, student loans, and payment plans. Discuss what that will look like down the road, as some of these options will have a future payment responsibility.

Turn everyday math into life skills with fun, guided online learning. You can start teaching kids as early as age 3. Preschoolers can understand that things cost money. You can start with saving small amounts in a clear jar for simple goals. At this stage, you need to build the foundation of financial literacy by introducing them to the idea of saving up. A good starting point, according to Capital One (2024), is $1 per week per age. So, if your child is 7 years old, they might receive $7 per week. However, the system matters more than the amount. Whenever you can, tie the money to contributions and teach them to divide it between spending, saving, and donations. The best way to teach kids the value of money is by making them earn it. Let them earn money through contributions and part-time jobs, and let them spend it and run out of it (within safe limits, of course). When money isn’t tied to effort, children tend to spend it without much thought. Yes. At around 10-12, you can open a joint savings account, and at 14-16, a checking account with a debit card. Having bank accounts will make financial concepts more concrete. This way, your child will have more freedom to manage their money, but also pressure to do it responsibly. Sit down together and calculate their income from work, contributions, allowances, and gift money. Map out how much they will spend that month and on what, and how much they want to save. It doesn’t have to be perfect on the first try, but it builds the habit of looking where the money will go before spending it. Some of the key money habits you can teach your kid are to earn before they spend, save consistently, even small amounts, pause and think before impulse purchases, and give intentionally. Also, kids and money work best together when you teach them that talking openly about money is a normal part of everyday life. How to teach subtraction to kids is not rocket science, especially if you know how and when to apply fun strategies like games, aids, and hands-on activities. As a Brighterly tutor working with kids myself, I’ve written this guide to explore the best methods of teaching subtraction to kids so that they can build a […] Feb 16, 2022 Math tricks for kids refer to mental workouts, like multiplying by 11 by adding digits. They can turn long calculations into quick mental shortcuts – and make numbers fun. This guide covers 20 easy math tricks, complete with step-by-step examples your child can try right now. Key Points Tricks like “Make 10” or breaking numbers […] Feb 22, 2022

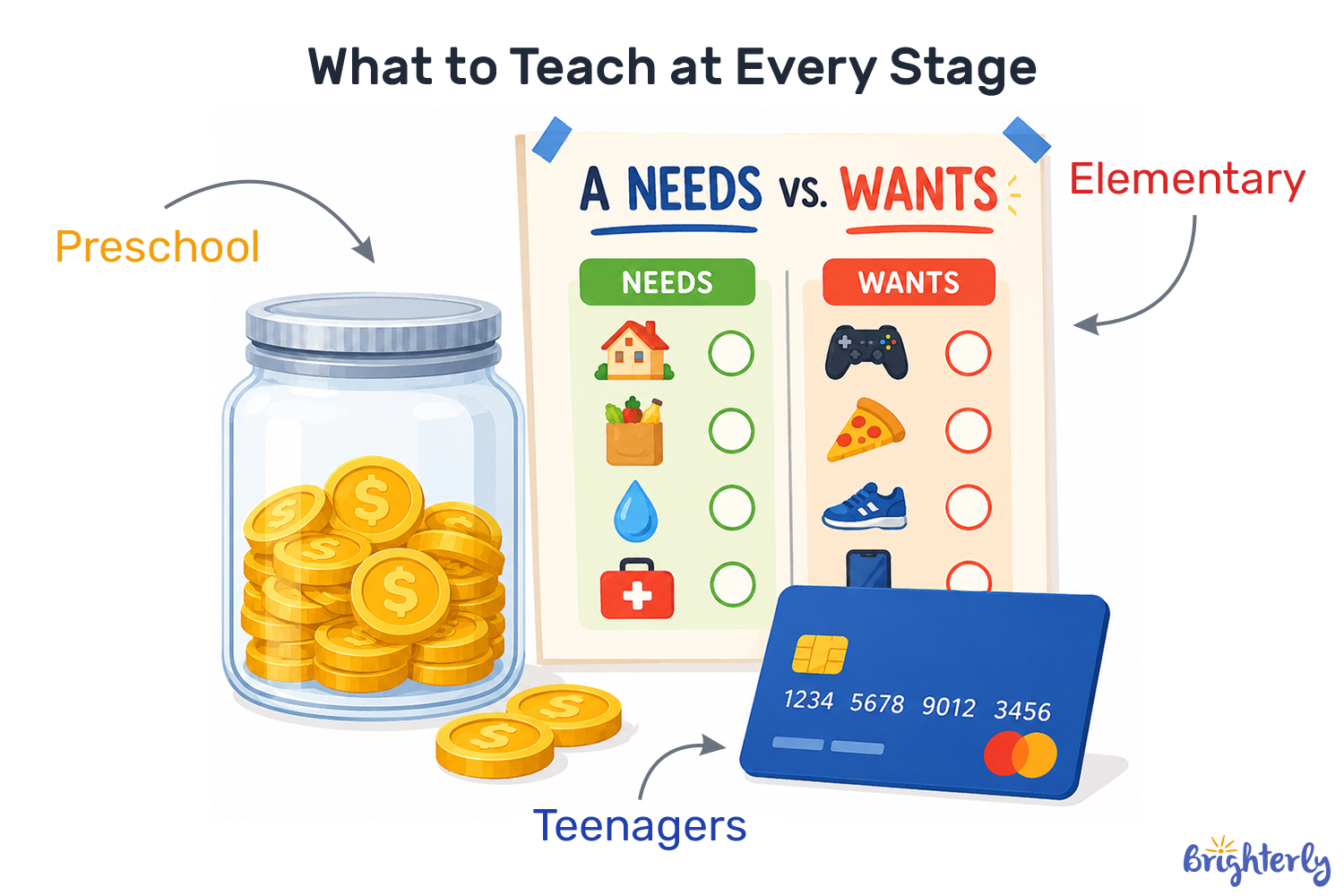

How to Teach Preschoolers About Money (Ages 3–5)

1. Use a Clear Jar for Savings

2. Show Them That Stuff Costs Money

3. Play Store at Home

4. Set an Example with Your Own Money Habits

Explore Brighterly Learning Experience

How to Teach Elementary School Kids About Money (Ages 6–10)

5. Teach Needs vs. Wants

6. Give Commissions, Not Allowances

7. Set a Savings Goal Together

8. Practice Opportunity Cost

9. Avoid Impulse Buys

10. Encourage Giving

Make Money Lessons Click

How to Teach Middle Schoolers About Money (Ages 11–13)

11. Open a Bank Account Together

12. Build a Simple Budget

13. Explain How Compound Interest Works

14. Introduce Basic Investing

15. Talk About Contentment and Delayed Gratification

How to Teach Teenagers About Money (Ages 14–18)

16. Encourage a Part-Time Job or Side Hustle

17. Open a Checking Account in Their Name

18. Explain the Danger of Credit Cards

19. Introduce the Roth IRA

20. Help Them Plan for College Costs

1:1 Learning with Experienced Math Tutors

Frequently Asked Questions

At What Age Should I Start Teaching Kids About Money?

How Much Allowance Should I Give My Child?

What Is The Best Way To Teach A Child The Value Of Money?

Should Kids Have Their Own Bank Account?

How Do I Teach My Teenager To Budget?

What Are Good Money Habits To Teach Kids Early On?

Math & reading from 1st to 12th grade

Looking for homework support for your child?

Choose kid's grade

Math & Reading for Grades 1–12

Build real confidence for your child with a Brighterly math or reading tutor.